March Insights

March Insights

1. Should you be paying tax on your side hustle?

Conventional approaches to work and earning an income are changing and with the cost of living ever rising, many now use various ways to make some extra cash outside of their main job.

HMRC have launched a new campaign aimed at clarifying whether you need to tell them about any side hustle earnings so you can avoid any nasty surprises.

The guidance looks at five different types of hustle. Here we briefly review them and what you need to know:

1. I’m buying or making things to sell

If you sell things you make, upcycle furniture to sell, or buy items to resell at a higher price, then HMRC would consider you to be trading.

2. I’ve making income from a side gig

Side gigs vary but might include providing car repairs, making deliveries, dog walking, gardening or tutoring. Although this work may be done in your spare time, if it’s regular and carries on for a few months, HMRC would consider it to be trading.

3. I work for myself doing multiple jobs

If you’re earning a living from doing several different jobs, then you could be trading and need to register as a sole trader.

4. I’m a content creator or influencer

What may have started as a hobby could have become an earner for you. For instance, if you get paid to do sponsored social posts for a brand, or you get ad income from your online videos or blog, then HMRC will consider you to be trading.

How much can you earn from trading before you need to tell HMRC?

If you earn £1,000 or less in a tax year, then you won’t pay any tax on it. However, if you earn more than £1,000 (or £3,000 from 2027/28) you need to complete a tax return and may need to pay tax. This £1,000 limit is a single allowance that applies to your combined trading income.

Some may suggest that if you sell less than 30 items a year you do not need to pay tax, however this is not correct. Online platforms are required to share some information with HMRC if you sell more than 30 items in a year, but that doesn’t mean you necessarily need to pay tax. You may also be due to pay tax if you sell less than 30 items. The key question is whether you have earned more than £1,000.

There is one other type of side hustle income that you might need to tell HMRC about, but this has some different rules to consider.

5. I rent out my property

It could be that you run a holiday let, rent a spare room, or rent out a property through an app. If you rent out a spare room, then that may be covered by the £7,500 rent a room scheme allowance. If you rent out a property that you don’t live in, then you also have a property allowance of £1,000, but if you receive more than that, then you need to pay tax on it.

2. Making Tax Digital for income tax

With just over a year to go before Making Tax Digital for Income Tax (MTD for IT) is mandated, now is the time to consider whether your business will be required to comply with the new requirements from 6 April 2026. MTD for IT will involve keeping your detailed accounting records in compatible software and sending quarterly digital reports to HMRC.

If you are a sole trader or run an unincorporated property business, and your ‘qualifying income’ is £50,000 or more in the 2024/25 tax year, you will be mandated into MTD for IT from 6 April 2026. If your qualifying income in 2023/24 was above or nearing £50,000, and you expect it to stay at around that level or increase for 2024/25, then there’s a good chance that you’ll be mandated.

HMRC are taking this approach. They’ve said that they’ll use 2023/24 returns (the deadline for which was 31 January 2025) to identify which taxpayers are likely to be mandated from 6 April 2026. They’ll be sending those taxpayers a letter in the coming months, advising them that they’re likely to be mandated and explaining why.

3. Plug-in van grant extended for another year

The Future of Roads Minister, Lillian Greenwood, has confirmed that the plug-in van grant will be extended for another year. Businesses can obtain grants of up to £2,500 when buying an eligible small van up to 2.5 tonnes and up to £5,000 for an eligible larger van up to 4.25 tonnes.

The grant is made available through the dealer or manufacturer as a discount on the purchase price when the van is purchased.

The government is also removing the requirement for additional training that is currently required for zero emission vans but not petrol or diesel ones.

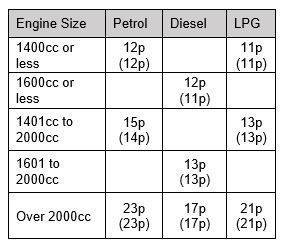

4. Advisory fuel rates for company cars

The table below sets out the HMRC advisory fuel rates from 1 March 2025. These are the suggested reimbursement rates for employees' private mileage using their company car.

Where the employer does not pay for any fuel for the company car these are the amounts that can be reimbursed in respect of business journeys without the amount being taxable on the employee.

Previous rates are shown in brackets and can be used for up to 1 month from the date the new rates apply.

Note that for hybrid cars, you must use the petrol or diesel rate and for fully electric vehicles the rate remains at 7p per mile.

Employees using their own cars

For employees using their own cars for business purposes, the Advisory Mileage Allowance Payment (AMAP) tax-free reimbursement rate continues to be 45 pence per mile (plus 5p per passenger) for the first 10,000 business miles, reducing to 25 pence a mile thereafter.

Input VAT

Within the 45p/25p AMAP payments, the amounts in the above table represent the fuel element. The employer can reclaim 1/6 of the fuel amount as input VAT provided the claim is supported by a VAT invoice from the filling station. So, for a 2500cc petrol-engine car, 4 pence per mile can be reclaimed as input VAT (23p x 1/6).

5. Business Rates Relief confirmed for 2025/26

A letter from the government’s Non-Domestic Rates Team to councils has confirmed the Business Rates Relief measures for 2025/26 announced at the 2024 Autumn Budget. Here’s a summary.

Standard and small business multipliers

This confirms that:

· The non-domestic rating multiplier will be 55.5p.

· The small business non-domestic rating multiplier will be 49.9p.

Relief for retail, hospitality and leisure properties

For retail, hospitality, and leisure properties, 40% relief (capped at £110,000) is available for 2025/26 under the Retail, Hospitality and Leisure Business Rates Relief scheme. Guidance has been published setting out the eligibility criteria. Local authorities are expected to include details of the relief to eligible ratepayers in their 2025/26 rates bills.

The £110,000 cap is per business and not per property. As has been the policy in previous years, businesses who would be eligible for relief above £110,000 if there were no cap in place, should be awarded relief up to the full value of £110,000.

What about private school charities?

The Non-Domestic Rating (Multipliers and Private Schools) Bill has passed the final stages in the House of Commons and is now working its way through the House of Lords. The measure to remove charitable rate relief from private school charities is subject to this legislation being enacted. It is still expected that the relief will be removed from 1 April 2025. However, local authorities have been told that they should not issue bills with the relief removed until after the law’s been enacted.

Edited by - Peter Burns - Senior Client Manager at England & Company